Bill Monreal

Bill Monreal 4 min read

Are My Clients at Risk? Why You Need a Cyber Audit

Worried your accounting firm might fail a cybersecurity check? Discover how a cyber audit protects your Ohio CPA firm from breaches and massive IRS...

I recently sat down with the managing partner of an Ohio CPA firm right in the middle of the spring tax rush. The tension in their office was thick enough to cut with a knife. Between chasing down missing W-2s and answering panicked client phone calls asking if dog food counts as a legitimate business expense, the absolute last thing on their mind was network security. But as someone who spends every day fighting cyber threats, it’s my opinion that tax season is exactly when your firm is the most vulnerable.

Hackers know you're distracted. They know your firm handles a massive volume of sensitive financial data, Social Security numbers, and bank account details. Threat actors specifically target accounting professionals because the potential payout is simply too high for them to ignore. Let's talk about the real threats you face and how you can stop them before they ruin your firm's hard-earned reputation.

I can't count the number of times I've seen a cleverly disguised email bypass a firm's standard spam filter. Just last month, I reviewed a phishing attempt that perfectly mimicked a well-known bank's secure document portal. It looked completely flawless. The attackers were trying to trick an accountant into entering their login credentials by claiming an urgent client wire transfer had failed.

For accounting firms, the risk here is staggering. You constantly interact with clients and financial institutions via email, which makes you incredibly susceptible to these scams. A hacker only needs to succeed once. If an employee clicks a malicious link and hands over their credentials, the attackers gain immediate access to client funds and business accounts. The fallout includes devastating financial losses and massive legal liabilities. You need to be deeply suspicious of every urgent email attachment you open.

Imagine walking into your office on April 10th, opening your laptop, and finding that every single client tax return file is locked. A digital ransom note sits on your desktop demanding payment in cryptocurrency to restore your access. I've witnessed the sheer panic this scenario causes firsthand, and it's truly heartbreaking.

Ransomware is malicious software that encrypts your organization's data until a ransom is paid. Cybercriminals love targeting CPAs with ransomware because your data is incredibly time sensitive. Missing a strict filing deadline is catastrophic for your clients. Attackers know you'll be tempted to just pay the ransom quietly to get back to work. However, paying the ransom is a terrible idea. There's no guarantee you'll get your data back, and you might find your stolen client data for sale on the dark web anyway.

A data breach is the ultimate nightmare for any organization dealing with confidential information. When unauthorized individuals access your private data, the results are often life-altering for your clients. Hackers use stolen tax filings and Social Security numbers to commit identity theft or file fraudulent tax returns on behalf of your clients.

One thing that constantly surprises me when auditing new clients is how much historical data they keep sitting in unprotected folders. I highly recommend auditing your shared drives right now. If you leave archived files exposed without proper encryption or strict access controls, you're serving up an all-you-can-eat buffet for cybercriminals. If your top clients start asking questions about your security posture, you need to learn how to provide the evidence they need to maintain their trust. You can also refer to the official IRS guidelines for safeguarding taxpayer data for additional regulatory compliance steps.

It's not always a shadowy hacker in a hoodie typing furiously in a dark basement. Sometimes, the biggest risk comes from inside your own walls. I've seen well-meaning employees cause massive breaches entirely by accident.

Insider threats happen when employees or contractors misuse their access to sensitive data. A common issue I see is staff members using their own unsecured devices to check work email or access client files from home. If an employee loses a personal phone that has access to your firm's data, you've got a serious problem on your hands. You must learn exactly how to secure those personal devices to prevent a disaster.

You simply can't afford to ignore these risks. Here's a practical plan to secure your firm today:

If you want a deeper understanding of these concepts, I highly recommend reading our comprehensive breakdown of cybersecurity essentials to ensure you're fully protected. Handling all of this on your own is incredibly overwhelming, which is why it makes sense to explore all aspects of managed services to see how a dedicated partner can take this burden off your shoulders.

Cybersecurity threats are evolving, and accounting firms are squarely in the crosshairs. Protecting your data is about more than just avoiding regulatory fines; it's about preserving the deep trust your clients place in you. You need a partner who intimately understands your unique regulatory requirements and daily operational stressors, a provider of managed services Cleveland businesses trust. Let's fix your security gaps before the next major tax deadline arrives.

4 min read

Worried your accounting firm might fail a cybersecurity check? Discover how a cyber audit protects your Ohio CPA firm from breaches and massive IRS...

5 min read

Missing your Written Information Security Plan? Learn why the IRS requires a WISP for accounting firms and how to protect your practice from heavy...

9 min read

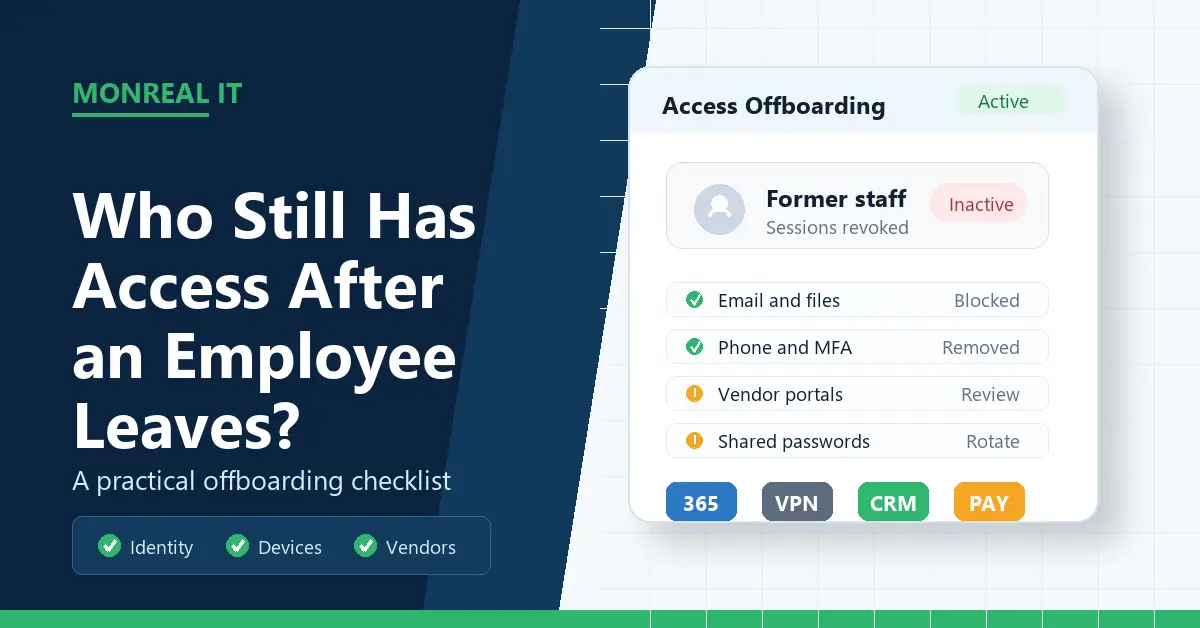

When an employee leaves, access can linger in apps, email, files, and vendors. Use this practical offboarding checklist to close the gaps.